Last modification

Update 11 June 2026: Publication of the Corporate Net-Zero Standard Version 2.0 (CNZS 2.0)

On 11 June 2026, the Science Based Targets initiative (SBTi) published the new Corporate Net-Zero Standard Version 2.0. This represents a comprehensive further development of the existing net-zero framework. The focus is shifting more strongly away from mere target-setting towards implementation, progress measurement and the credible integration of climate targets into corporate strategy and governance. New elements or those given greater emphasis include separate target structures for Scope 1, Scope 2 and Scope 3, transition plans, continuous progress assessment, and Ongoing Emissions Responsibility (OER) as a supplementary framework for addressing ongoing emissions. The CNZS 2.0 will be mandatory for companies from 31 January 2028 for all target achievements. More information

The driving force behind SBTs is the Science Based Targets initiative (SBTi). It is a joint initiative of CDP, the UNGC, WRI and WWF, which develops methodologies and criteria for effective climate protection in companies and validates corporate targets. The SBTi has also drawn up a Net-Zero Standard for companies. In June 2026, the SBTi published the Corporate Net-Zero Standard 2.0.

The SBTi’s Corporate Net-Zero Standard provides companies with a science-based framework for setting short- and long-term climate targets and planning their transition to net zero. It sets out how companies can reduce emissions across their value chain and achieve net-zero by 2050 at the latest.

Version 2.0 represents a comprehensive update to the standard. The focus is no longer solely on setting ambitious targets, but increasingly on their implementation, measuring progress and integrating them into governance, strategy and operational decision-making processes. myclimate supports companies in developing short- and long-term science-based targets.

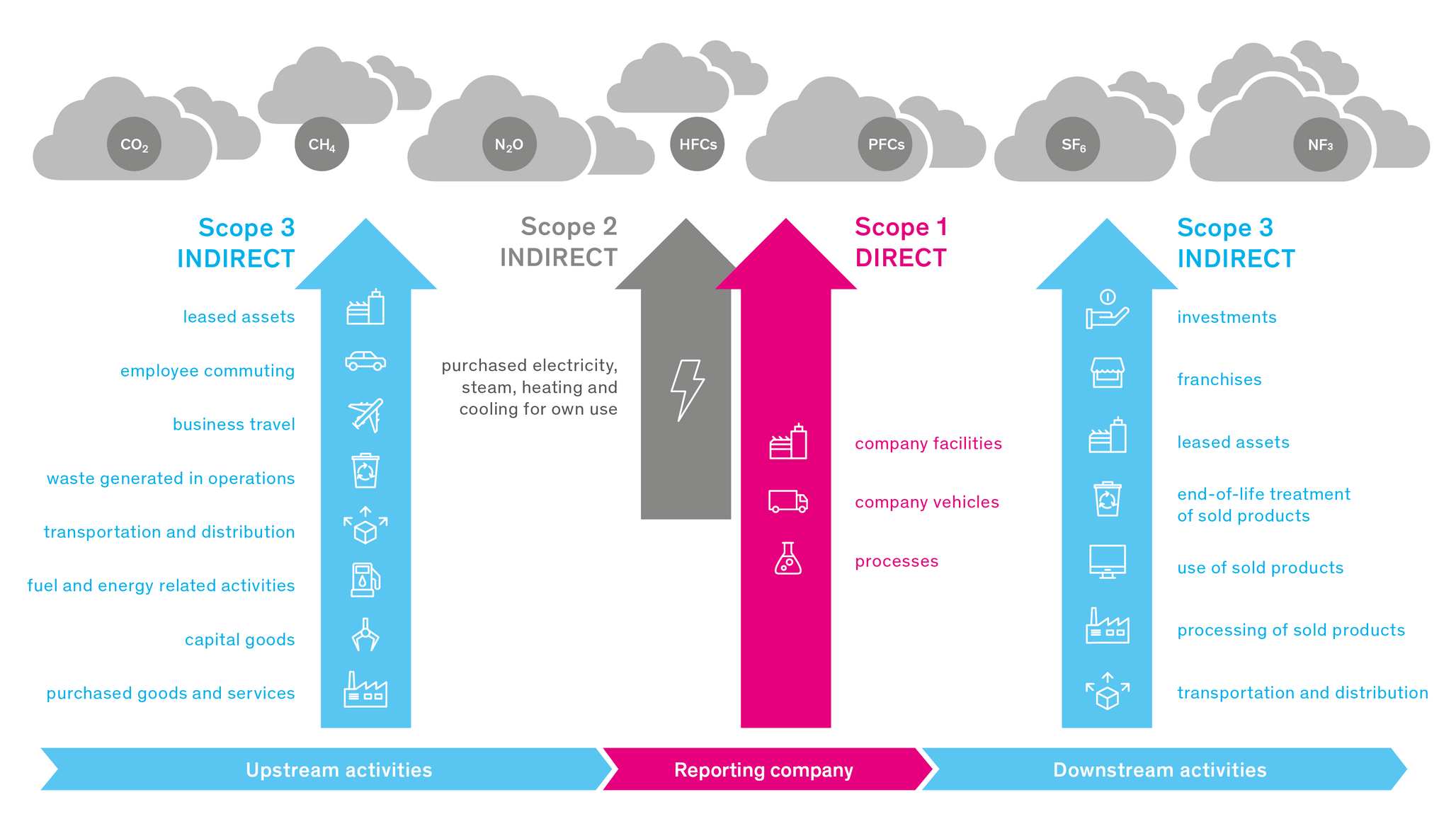

To effectively limit global temperature rise to 1.5 °C, swift and far-reaching measures are needed to reduce emissions across the value chain. That is why the Net-Zero Standard covers a company’s entire value chain, encompassing Scope 1, Scope 2 and Scope 3 emissions. The inclusion of indirect emissions (Scope 2 and Scope 3) requires most companies to achieve deep decarbonisation of at least 90 per cent in order to meet the Net-Zero Standard.

Companies wishing to align their climate targets with the Net-Zero Standard must set both short-term and long-term, science-based targets. This means short-term targets are needed to reduce emissions as quickly and effectively as possible. A new feature is the introduction of short-term cycles, which help to carry out regular assessments of progress, implementation barriers and measures to overcome them; as well as setting new targets before or at the end of a cycle. This ensures a continuous focus on net-zero pathways, even where gaps exist between emissions and targets. In addition, long-term targets are needed that enable net-zero to be achieved by 2050, and under which companies invest in climate protection projects with carbon removal capabilities for any residual emissions that cannot be avoided.

Most companies will need to reduce at least 90 per cent of their emissions by 2050. Even if a company sets itself long-term and ambitious reduction targets and makes efforts to meet them, it is only considered a net-zero company once it has achieved those targets.

The Net-Zero Standard also recommends that companies make investments outside the value chain to mitigate climate change – for example, through climate protection projects. However, these investments should not be seen as a substitute for far-reaching emissions reductions within the company. Rather, they complement the company’s established and ambitious climate targets, thereby underlining its commitment to achieving net zero by 2050.

The new standard introduces the following changes in particular:

New or revised company categories, including adaptations to the definition of SMEs.

A refined target structure with separate targets for Scope 1 and Scope 2, as well as an adapted Scope 3 approach with a stronger focus on material emissions categories.

Greater integration of net-zero targets into governance and corporate strategy.

Transition plans as a key component of implementation: companies are required to set out the measures and dependencies they intend to use to achieve their targets.

Introduction of an implementation hierarchy to help companies prioritise decarbonisation measures within their own operational processes and value chains.

Continuous progress assessment: Companies should make progress visible, and identify and address gaps and obstacles.

An expanded role for financing climate protection, including the introduction of the Ongoing Emissions Responsibility (OER) recognition scheme.

The revision is largely based on feedback from companies in the field. Many organisations have set their climate targets in good faith, but have encountered structural challenges in implementing them, in particular:

The aim of CNZS 2.0 is therefore to provide a more practical, implementation-oriented and, at the same time, credible framework for the net-zero transition.

Ongoing Emissions Responsibility (OER) describes a framework through which companies can take responsibility for ongoing or residual emissions on the path to net zero. This may include supplementary climate finance.

It is important to make a clear distinction: OER does not replace emissions reductions within a company’s own value chain. Companies must continue to work consistently towards reducing their Scope 1, Scope 2 and relevant Scope 3 emissions. OER can complement a credible net-zero strategy by enabling companies to take on additional responsibility for emissions that continue to arise during the transition.

Companies that already have SBTi targets do not automatically have to take immediate action. Existing targets remain in place; revalidation or resubmission, based on the latest information, will be required either upon reaching the target year or at the mandatory five-year review – whichever comes first. However, companies should plan for the transition to Version 2.0 at an early stage for the next target cycle.

Companies with planned SBTi targets should assess which requirements of the new standard are relevant to them. Of particular importance are classification into the appropriate company category, the implications for Scope 1 to 3 targets, governance requirements and transition plans.

The question of what role OER play in their own climate strategy may also be of interest.

Version 2.0 was published on 11 June 2026. From 31 January 2027, Version 2.0 may be used for target submissions. Companies may continue to submit targets to SBTi Services in accordance with version 1.3.1 until the end of January 2028. From 31 January 2028, version 2.0 will be mandatory for all target submissions.

According to the information currently available, companies and financial institutions have until 31 January 2027 to commit to setting separate short-term and/or net-zero targets.

myclimate helps companies to assess the implications of the Corporate Net-Zero Standard 2.0 and to define appropriate next steps. This includes developing or updating science-based targets, integrating them into a holistic climate strategy, planning their implementation, and incorporating additional financing for climate protection as part of a credible net-zero strategy.

Would you like to know what the new Corporate Net-Zero Standard 2.0 means for your company? Please contact us – we’d be happy to help you assess the implications and identify possible next steps.